Uncategorized

قصر الإمارات يعين مديرًا جديدًا لقسم المأكولات والمشروبات

أبوظبي – وينك

أعلن قصر الإمارات، الفندق الفاخر من فئة خمس نجوم في أبوظبي، عن تعيين السيد توم كوجي مديرًا جديدًا لقسم المأكولات والمشروبات.

ويتمتع توم بخبرة واسعة تفوق 12 عامًا في مجال إدارة قسم المأكولات والمشروبات. فقبيل انضمامه إلى قصر الإمارات، تولى إدارة قسم المأكولات والمشروبات في فندق لاندمارك ماندارين أوريانتال في هونغ كونغ. وبدايةً في عام 2016، تم تعيينه مساعدًا لمدير قسم المأكولات والمشروبات في إدارة المشاريع ذاك العام، الأمر الذي ساهم في تنمية شغفه بالأفكار والمشاريع المتعلقة بالمأكولات والمشروبات. كما كان أيضًا عضوًا في الجيل الأول من لجنة العلميات الموازية (POPCO) لدى ماندارين أورينتال في الفترة ما بين العامين 2017 و 2019.

وفي عام 2014، شغل توم عدة مناصب في مختلف الأقسام والفنادق، حيث تمرن على إدارة قسم المأكولات والمشروبات في فندق “ماندارين أوريانتال هايد بارك ” في لندن، وتولى الإشراف على مرحلة ما قبل الافتتاح للاونج “روزبيري” لشاي الظهيرة والمشروبات الفاخرة.

كما عمل توم في العديد من دول العالم كفرنسا، وهولندا، ونيوزيلندا، والمملكة المتحدة، وهونغ كونغ، الأمر الذي أتاح له الانخراط في الكثير من المشاريع وأكسبه خبرةً عميقة في مجال إدارة وتنفيذ المشاريع والأفكار المتعلقة بقسم المأكولات والمشروبات بشكل رياديّ فعّال. وسيعمل توم على توظيف خبراته في تحقيق أعلى معايير الجودة ومنح ضيوف القصر أفضل التجارب الذوقية على الإطلاق.

The personal‑loan market has been on a rollercoaster over the past decade, but data from LendingTree’s 2026 statistics report shows that the ride is gaining momentum again. In the fourth quarter of 2026 alone, American borrowers carried $276 billion in personal‑loan debt—up a solid 10% from the previous year and a staggering $25 billion higher than the 2026 figure.

While mortgages and auto loans still dominate consumer debt, personal loans now account for 1.5% of all outstanding consumer debt—a figure that has barely changed since the Great Recession’s peak in 2009. Yet the sheer volume of borrowers—26.4 million as of Q4 2025—indicates a growing appetite for installment credit that can be tailored to a wide range of needs.

To help readers navigate this expanding landscape, we’ve pulled together the latest data, industry insights, and practical tips from top lenders—including a quick look at how JetzLoan fits into the picture.

Borrower Demographics: Who’s Taking Out Personal Loans?

Personal loans are no longer a niche product reserved for high‑credit borrowers. The data shows that 51% of users take out a loan to consolidate debt, while another 10% use it for everyday expenses such as medical bills or home repairs.

- Credit Score Range: Borrowers with scores above 680 tend to secure rates under 25%, whereas those below 620 often face APRs exceeding 30%. Source

- Loan Amount: The average loan is $11,699, with a range that can stretch from $5,000 to over $50,000 depending on lender and credit profile.

- Term Length: Most borrowers choose terms between 36 and 60 months, striking a balance between manageable monthly payments and total interest costs.

The rise in loan volume coincides with the proliferation of online lenders that offer rapid approvals—sometimes within minutes—and same‑day disbursement. This convenience factor has been especially appealing to consumers looking for quick solutions to unexpected expenses.

Interest Rates: How Do They Stack Up?

APR trends have shifted dramatically in recent years. For borrowers with excellent credit (720+), the average APR hovers around 15%, comparable to premium credit‑card rates. Those with fair or subprime scores see rates climb into the high‑20s and low‑30s.

| Credit Score Range | Avg. APR | Avg. Loan Amount |

|---|---|---|

| 720+ | 15.08% | $20,236 |

| 680‑719 | 23.46% | $17,475 |

| 660‑679 | 27.20% | $14,195 |

| 640‑659 | 28.97% | $12,615 |

| 620‑639 | 30.30% | $11,973 |

| 580‑619 | 31.10% | $11,486 |

| 560‑579 | 31.84% | $11,187 |

| Below 560 | 30.40% | $11,447 |

These figures come from LendingTree’s user data for Q4 2025 and illustrate how lenders price risk: the better your credit, the more favorable the terms.

Fees That Can Add Up

Beyond APRs, borrowers must watch out for origination fees, which can range from 1% to 10% of the loan amount. Some lenders offer “no‑fee” promotions, but those often come with higher rates or stricter eligibility criteria.

- Origination Fee: Typically 1–5%, deducted from the disbursed amount.

- Prepayment Penalty: Rare in consumer loans, but some contracts still impose a fee for early payoff.

- Late Payment Fees: Vary by lender; can be as high as $35 per missed payment.

When comparing offers, it pays to calculate the effective annual rate (EAR), which accounts for both interest and fees. A seemingly low APR may hide a higher EAR if fees are steep.

The Rise of Digital Lenders: JetzLoan’s Place in the Market

While traditional banks still dominate the high‑credit segment, fintech companies have carved out niches by offering flexible terms, streamlined applications, and competitive rates for subprime borrowers. JetzLoan exemplifies this trend.

Key features of JetzLoan include:

- Fast Approval: Most applications receive a decision within 24 hours, thanks to automated underwriting algorithms.

- Flexible Repayment Plans: Borrowers can choose monthly or bi‑weekly schedules, which can shave months off the loan term and reduce interest.

- No Hidden Fees: JetzLoan advertises a flat fee of 2% for all loans, making it easier to compare offers side‑by‑side.

According to LendingTree’s data set, fintech lenders now represent nearly 35% of the personal‑loan market, a figure that has been steadily climbing since 2018.

How to Evaluate a Fintech Offer

When considering an online lender like JetzLoan, keep these checkpoints in mind:

- APR vs. EAR: Always calculate the effective rate to see the true cost.

- Customer Reviews: Check BBB ratings and independent review sites for service quality.

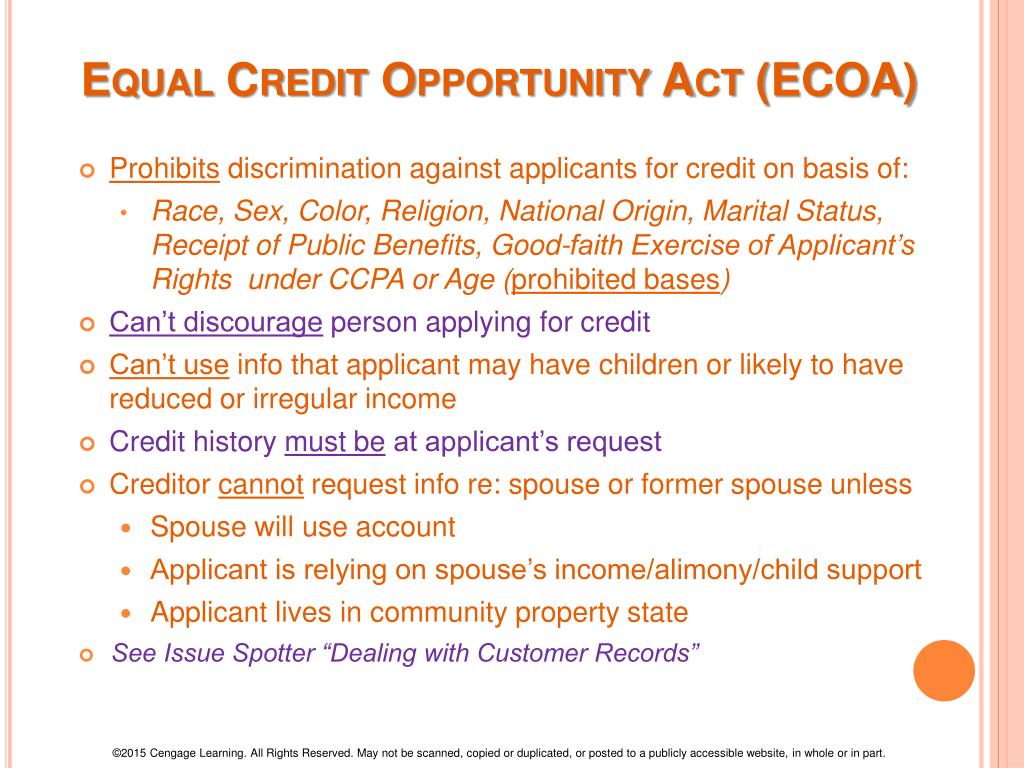

- Regulatory Compliance: Verify that the lender is registered with the CFPB and follows ECOA guidelines.

By doing a quick comparison of rates, terms, and fees across multiple platforms—including JetzLoan—you can secure the best deal for your financial situation.

Delinquency Trends: What the Numbers Tell Us About Risk

The delinquency rate for personal loans—defined as 60 days or more past due—stands at 3.99% in Q4 2025, up from 3.57% a year earlier. While this figure is higher than that of auto or mortgage loans, it remains lower than the average credit‑card delinquency (2.58% for 90+ days).

- High‑Risk Borrowers: Those with scores below 600 are more likely to miss payments.

- Economic Factors: Recent inflation and labor market shifts have contributed to a modest uptick in delinquencies.

- Lender Response: Many lenders now offer hardship programs, such as payment deferrals or restructuring options, to reduce defaults.

For borrowers, staying ahead of potential financial stress—by maintaining an emergency fund and monitoring credit scores—can mitigate the risk of falling into delinquency.

Industry Response: Regulatory Changes and Consumer Protections

The Consumer Financial Protection Bureau (CFPB) has recently rolled back certain consumer‑credit rules, sparking debate over how these changes might affect borrower protections. Critics argue that weaker regulations could open the door to predatory practices, especially for subprime borrowers who rely on online lenders.

- State-Level Oversight: Some states have stepped in with stricter licensing requirements for fintech companies.

- Consumer Advocacy Groups: Organizations like the National Consumer Law Center are monitoring the impact of regulatory rollbacks.

As the landscape evolves, borrowers should remain vigilant and seek transparent terms from any lender—whether a traditional bank or a digital platform like JetzLoan.

How Personal Loans Fit Into Your Broader Financial Strategy

Many consumers turn to personal loans for debt consolidation because it can lower overall interest costs and streamline monthly payments. However, the strategy’s success hinges on disciplined repayment and avoiding new high‑interest debt.

- Consolidation Benefits: A single payment reduces administrative hassle; a lower APR saves money over time.

- Potential Pitfalls: If the loan rate is higher than existing credit cards, consolidation may backfire.

- Alternatives: Balance‑transfer credit cards or secured personal loans can sometimes offer better terms for specific use cases.

Financial planners often recommend using a personal loan as part of a broader debt‑management plan that includes budgeting, emergency savings, and long‑term investing.

Real-World Example: A Mid-Career Professional’s Journey

Sarah, a 38-year-old marketing manager with a credit score of 680, faced $15,000 in credit‑card debt carrying an average APR of 22%. She applied for a personal loan through JetzLoan and secured a 5% APR over 48 months. By consolidating her balances into one lower‑rate payment, Sarah reduced her monthly outflow from $520 to $310—a savings of $210 that she redirected into retirement contributions.

Her experience underscores the importance of comparing rates across platforms, verifying fees, and aligning loan terms with personal financial goals.

The Road Ahead: Forecasting Personal‑Loan Growth

Analysts predict that personal‑loan debt will continue to rise, driven by consumer demand for flexible financing options. Projections estimate a 7–8% annual growth rate over the next five years, assuming stable economic conditions and continued digital adoption.

- Technology Adoption: AI underwriting models are expected to further reduce approval times.

- Regulatory Environment: Ongoing policy debates could reshape lender practices and borrower protections.

- Consumer Behavior: Post‑pandemic shifts toward online shopping and remote work may increase the need for short‑term, low‑interest credit.

For borrowers, staying informed about market trends and maintaining a healthy credit profile will be key to navigating this evolving landscape.

Key Takeaways for Consumers

- Do Your Homework: Compare APRs, fees, and terms across lenders—traditional banks, online platforms, and fintech companies like JetzLoan.

- Understand the Full Cost: Use the effective annual rate to gauge true borrowing expenses.

- Plan for Repayment: Align loan terms with your income flow and long‑term financial goals.

By staying proactive and informed, borrowers can harness personal loans as a powerful tool—whether it’s consolidating debt, covering unexpected expenses, or investing in future opportunities.

The past year has seen a steady rise in unsecured personal loan activity, with originations leaping 18% year‑over‑year in the first quarter of 2026. This uptick comes amid a broader backdrop of measured credit growth and declining delinquency rates across consumer borrowing categories. The data suggests that borrowers are becoming more disciplined, even as they continue to lean on credit for everyday expenses.

Bankrate’s recent coverage on low‑interest personal loans highlights how consumers can capitalize on favorable market conditions. By comparing offers from multiple lenders and understanding the factors that drive rates—credit score, debt‑to‑income ratio, employment status—a borrower can secure a loan with terms that fit their financial goals.

In light of these trends, many are turning to online platforms that streamline the application process while offering competitive rates. One such platform is Loan Now, which provides a quick pre‑qualification step and personalized rate estimates before you commit to an application.

How the Market Is Evolving for Personal Loan Seekers

The TransUnion Credit Industry Insights Report for Q2 2026 shows that unsecured personal loan balances hit a record $257 billion, yet the growth in balances has slowed compared to previous years. This moderation indicates borrowers are borrowing more cautiously while still taking advantage of available credit.

Delinquency rates have also softened. The 60+ days‑past‑due (DPD) delinquency rate fell to 3.37%, marking a third consecutive quarter of improvement. Credit unions and online lenders alike are witnessing this shift as consumers become more mindful of repayment schedules.

- Originations: 18% YoY increase in Q1 2025

- Balances: $257 billion record high

- 60+ DPD delinquency rate: 3.37%

These figures paint a picture of a credit market that is both robust and resilient, even as economic uncertainties loom.

The Role of Credit Scores in Securing Favorable Terms

A strong FICO score remains the most reliable lever for obtaining low interest rates. Lenders typically reserve the best offers for borrowers scoring above 800, but those with scores between 670 and 749 can still access competitive terms if they maintain a healthy debt‑to‑income ratio.

Bankrate’s article on qualifying for low‑interest personal loans emphasizes that lenders look beyond just credit score. Employment stability, income level, and the overall mix of existing credit accounts all factor into the final rate determination.

| Score Range | Typical APR | Common Loan Term |

|---|---|---|

| 800+ | 3.0%–4.5% | 36–60 months |

| 670–799 | 4.5%–6.5% | 48–72 months |

| Below 670 | 7.0%–10.0% | 60+ months |

The key takeaway? Even if your score isn’t in the “super‑prime” bracket, a well‑managed credit profile can still open doors to reasonable rates.

Pre‑Qualification: A Risk‑Free First Step

Before diving into a formal application, most lenders offer a pre‑qualification process that checks your credit without impacting your score. This step allows you to gauge potential interest rates and monthly payments while comparing offers from multiple institutions.

Bankrate notes that pre‑qualification typically requires only basic information—name, address, income estimate—and no hard inquiry. By running this quick check with at least three lenders, you can identify the most favorable terms before making a final decision.

- What to Expect: Rate estimates, eligibility snapshot

- How Long It Takes: 5–10 minutes online

- Result: No credit score impact

Once you’ve narrowed your options, the next step is a full application. This will involve a hard inquiry and may require documentation such as pay stubs or bank statements.

Why Online Lenders Are Rising in Popularity

The convenience of digital platforms cannot be overstated. From instant decision notifications to e‑signature capabilities, online lenders streamline the entire borrowing process.

Platforms like Loan Now provide a seamless experience: users can upload documents via secure portals, receive real‑time updates on application status, and even lock in rates before final approval. This level of transparency builds trust and speeds up the time to disbursement.

Moreover, many online lenders maintain competitive fee structures—some waive origination fees entirely—making them an attractive alternative to traditional banks.

Managing Your Loan Responsibly

A personal loan’s true value lies in its ability to help you consolidate debt, cover unexpected expenses, or invest in opportunities. However, responsible use is essential to avoid falling into a debt cycle.

Bankrate advises borrowers to set up autopay where possible; this not only guarantees on‑time payments but often comes with a discount on the interest rate.

- Set a Budget: Allocate a fixed amount for monthly payments

- Monitor Your Credit: Check reports quarterly to spot errors

- Pay Early: If you can, paying off the loan ahead of schedule saves on interest

By following these practices, borrowers can enjoy the flexibility of a personal loan while safeguarding their financial health.

What’s Next for the Personal Loan Market?

With mortgage rates expected to remain relatively steady through the remainder of 2026, personal loans are poised to fill gaps left by other credit products. As consumers become more adept at navigating credit landscapes, we anticipate a continued rise in disciplined borrowing behavior.

For those looking to explore loan options today, platforms like Loan Now offer an accessible entry point into the market. Whether you’re consolidating debt or funding a new venture, understanding the current environment can help you make informed decisions.

To learn more about how to evaluate loan offers and manage your credit responsibly, visit Bankrate’s guide on qualifying for low‑interest personal loans. For a deeper dive into the latest consumer credit trends, refer to InvestmentNews’s coverage of U.S. consumer credit.

Wer in Hannover intime Begegnungen sucht, hat die Chance, mit verschiedenen Personen sich zu treffen. Hier erfahren Sie, worauf man bei Sex Treffen in Hannover achten sollte, damit man die idealen Kontakte ergattert und wie ein Dating Portal dabei leisten kann.

Das Besondere an Sex Treffen in Hannover

Die Stadt weckt mit ihrer Vielfalt großes Interesse bei Singles und Paaren. Dating Webseiten aus Deutschland bieten eine großartige Plattform, um einfach Sex Treffen in Hannover zu planen.

In Hannover vereinen sich attraktive Locations für Anfänger und erfahrene Liebhaber.Ob in Bars, Clubs oder via Webportale: Sie können, Ihre Wünsche zu verwirklichen.

Sex Treffen Hannover: Kontakte finden und nutzen

Wer ein Treffen fürs Sex sucht, sollte mit Strategie handeln. Eine Deutsche Dating-Seite kann Ihrer Suche einen großen Schub verleihen. Wichtig ist dabei, auf Diskretion, Verlässlichkeit und echte Profile zu achten.

Online-Plattformen bieten den großen Vorteil, dass Sie vielfältige Profile einsehen können.Sie können gezielt nach Leuten suchen, die Sex Treffen in Hannover anbieten und Ihre Wünsche teilen.

Natürlich ist auch die Kommunikation wichtig.Achten Sie auf ehrliche Angaben und echte Bilder. So sparen Sie Zeit und finden passende Begegnungen leichter.

Deutsche Dating-Seite vs. klassische Sex Treffen Seite: Was ist besser?

Sex Treffen Seiten sind spezialisiert intensiver auf schnelle, unkomplizierte Verabredungen und sexuelle Begegnungen. Die Wahl zwischen beiden ist oft eine Frage der Prioritäten.

Wenn Sie nach schnellen Kontakten suchen, könnten spezialisierte Sex Treffen Seiten effektiver sein. Sie bieten direktere Kontaktmöglichkeiten ohne großen Aufwand.

Diese Seiten sind ideal, um flexibel zu bleiben und auch andere Beziehungstypen zu erkunden. Sie sind meist gut moderiert und bieten zahlreiche Funktionen.

Worauf sollte ich bei einer Sex Treffen Seite achten?

Vertrauen ist das wichtigste Kriterium für eine Sex Treffen Seite. Überprüfen Sie, ob die Seite sichere Datenübertragung und einen gewissen Verifizierungsprozess bietet. Ohne diese Funktionen sind Risiken hoch.

Eine nutzerfreundliche Oberfläche erleichtert Ihnen den Einstieg und die sex date hannover Nutzung. Wenn die Suche nach Sex Treffen aufwendiger wird, verliert man schnell das Interesse. Auch eine gute mobile Version der Seite ist heute wichtig.

Funktionale Filter ermöglichen die schnelle Eingrenzung auf das gewünschte Profil. Ob Alter, Interessen oder bestimmte Vorlieben, je genauer, desto besser.

Recherchieren Sie vor der Anmeldung, wie andere User die Seite bewerten. Das gibt Aufschluss über die Qualität und kann böse Überraschungen vermeiden.

Fazit: Sex Treffen in Hannover erfolgreich gestalten

Sex Treffen in Hannover bieten zahlreiche Chancen für leidenschaftliche Begegnungen. Wer gezielt sucht, findet einfach und sicher sein Sex Treffen in Hannover.

Kombinieren Sie verschiedene Plattformen, um das beste Ergebnis zu erzielen. Vorsicht und Diskretion gehören zu jedem Treffen dazu, um Enttäuschungen zu vermeiden.

Mit etwas Geduld und diesen Tipps wird Ihr Sex Treffen in Hannover ein echtes Highlight. Viel Erfolg bei der Suche!

فنادق ومنتجعات كونستانس ترتقي بتجارب العافية في جزر المحيط الهندي

11 سبباً لزيارة مراكز التسوق التابعة لماجد الفطيم خلال مفاجآت صيف دبي 2026

نادي جيه أيه للرياضة والرماية يقدّم مجموعة تجارب جولف وتنس وبادل استثنائية هذا الصيف

-

اوتو كار6 years ago

تويوتا كورولا 2020 مواصفات السيارة بالكامل

-

أخبار سياحة6 years ago

تأشيرة الى خمس مناطق سياحية بسطيف الجزائري (صور)

-

أخبار سياحة6 years ago

قسنطينة مدينة الجسور المعلقة بالجزائر (صور)

-

أخبار سياحة6 years ago

أخبار سياحة6 years agoقمرت أجمل مدن تونس.. طبيعة خلّابة وحياة راقية.. صور وفيديو

-

فنادق ومطاعم 4 years ago

مطاعم تونس العاصمة: تعرف علي افضل مطاعم تونس العاصمة 2022

-

أخبار سياحة6 years ago

9 من أفضل المنتجعات الصحراوية في الإمارات: من الربع الخالي إلى دبي (صور)

-

أخبار سياحة5 years ago

منتجع ارض الاساطير في انطاليا، ذا لاند اوف ليجندز

-

فنادق ومطاعم 6 years ago

منتجع أنانتارا الجبل الأخضر سلطنة عُمان وجهتك الآمنة

You must be logged in to post a comment Login